How to draw up an advance report according to the standard system. USN. Object "income". Advance report. Advance payment to supplier for goods

Simplified tax system: recognition of income and expenses (1C Accounting 8.3, edition 3.0)

2016-12-08T11:39:01+00:00Today we will look at a topic that raises perhaps the largest number of questions from novice (and not only) accountants - the procedure for recognizing income and expenses under the simplified taxation system (STS) in the 1C: Accounting 8 program family.

We will consider examples in 1C: Accounting 8.3 (edition 3.0). But in the “two” everything works the same way.

A short excursion into theory

We are interested in filling out the book of income and expenses (KUDIR). In this wonderful book:

- Column 4 is the “Total Income” column

- column 5 is “Accepted income”

- column 6 is the column “Total expenses”

- column 7 is “Accepted expenses”

We are primarily interested in columns 5 and 7. They influence the amount of the single tax we pay.

There are two main modes in "simplified":

- income (column 5)

- income (column 5) minus expenses (column 7)

To calculate the single tax, in the first case we simply multiply the amount of income by 6%, and in the second case we multiply the difference between income and expenses by 15%.

That's all in a nutshell.

Correctly calculating income and expenses is the most difficult task. Already based on the presence of four columns “total income” and “accepted income”, “total expenses” and “accepted expenses”, it turns out that not all income and expenses can be taken to calculate the tax.

You need to be able to correctly determine the moment of recognition of income or expense. Under the simplified tax system, it is mandatory to use cash method.

Under the cash method, the date of receipt of income is the day the funds are received in bank accounts or at the cash desk. And it doesn’t matter whether it’s an advance or payment. The money has arrived - income has been received, and therefore immediately falls into columns 4 and 5.

As you can see, with income everything is extremely simple. Any receipt of money (to the cash register or to the current account) falls into general and recognized income, on which tax must be paid.

With expenses, everything is somewhat more complicated.

For recognition expenses for purchasing materials- it is necessary to reflect the fact of their receipt and payment.

For recognition expenses for payment of services provided to us- it is necessary to reflect the fact of their provision and payment.

For recognition expenses for purchasing goods for subsequent resale - you need to reflect the fact of their receipt, payment and sale.

For recognition labor costs- you need to reflect the fact of its accrual and payment.

When paying via expense reports- in addition to the above conditions, it is required to reflect the fact of issuing money to the accountable person.

As you can see, for many of the listed situations there are several conditions for recognizing expenses. And these conditions can be met in different orders. In this case, the moment of recognition of the expense will be considered last condition met.

Advance payment from buyer to bank

The buyer transferred money to our bank account as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into “Total Income” (column 4) and “Accounted Income” (column 5):

bank receipt -> column 4 + column 5

We issue a statement (receipt to the current account) for 2000 rubles from the buyer of Magic Hind LLC:

We post and open document transactions (DtKt button). We see that the payment amount was assigned to 62.02 - everything is correct, because this is an advance:

Immediately go to the second tab “Income and Expense Accounting Book”. It is here that payment amounts are posted (or not posted) in the KUDIR columns. We see that the 2000 rubles received immediately fell into columns 4 and 5:

Advance from the buyer at the checkout

With a cash register, everything is similar to a bank. The buyer paid money to the cash register as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into columns 4 and 5:

cash receipt -> column 4 + column 5

We issue a cash receipt order (cash receipt) from the buyer "Svergunenko M. F." for the amount of 3000 rubles:

We post the document and go to its postings (DtKt button). We see that the payment amount was assigned to 62.02 - everything is correct, because this is an advance:

We immediately go to the “Income and Expenses Accounting Book” tab and see that our entire amount falls into columns 4 and 5:

Payment to the supplier for services rendered

Let's move on to expenses. This is where things get more interesting. But not in the case of payment for services provided to us. We just need to enter the act of provision of services and its payment into the program, then the act itself (according to the cash method) will not make any marks in the KUDIR columns, but the bank statement will immediately post the amount of payment in columns 6 and 7:

certificate of provision of services -> will not do anything

payment by bank -> column 6 + column 7

We enter into the program a certificate of provision of services from the supplier Aeroflot in the amount of 2500:

We post the document and go to its postings (DtKt button). We see that expenses (26th invoice) were attributed to 60.01 - everything is correct:

We do not see the “Book of Income and Expenses Accounting” bookmark, which means that the indicated 2500 did not fall into any of the KUDIR columns. Go ahead.

The next day we submit a statement of payment for the services provided to us:

We carry out the statement and look at its postings. We see that the payment amount was applied to 60.01:

We immediately go to the “Income and Expenses Accounting Book” tab and see that the paid 2,500 finally fell into columns 6 and 7:

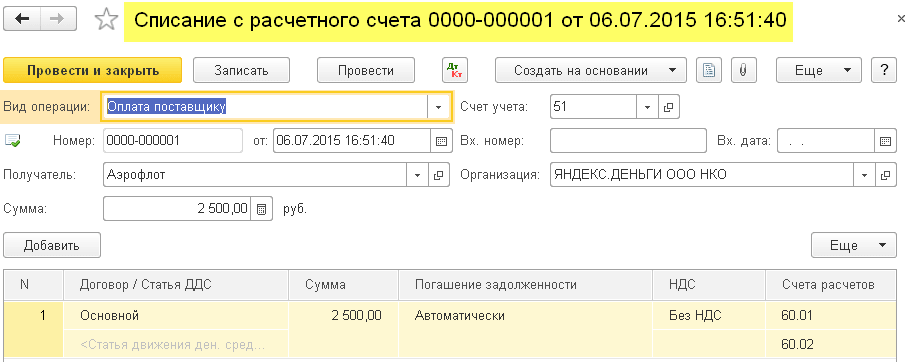

Advance payment to the supplier for the provision of services

What if we made an advance payment to the supplier for services provided (advance payment)? And only then they issued an act of provision of services. Schematically it will look like this:

payment by bank -> fill in column 6

act of provision of services -> fill out column 7

Let’s enter into the program a bank statement (our advance payment to the supplier) in the amount of 4500:

Let’s post the document and open its postings (DtKt button). We see that the amount fell on 60.02 - everything is correct, because this is an advance:

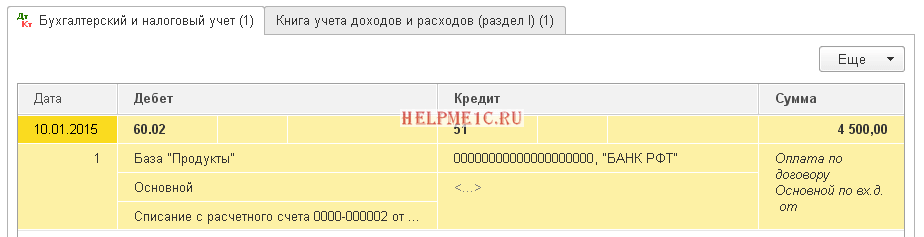

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the advance amount is included only in column 6:

And it is right. According to the cash method, in column 7 (accepted expenses), we will be able to take this amount only after entering the certificate of provision of services. Let's do it.

We will add an act of service provision to the program the next day:

Let's go through the document and look at the postings:

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount finally falls into the seventh column:

Payment to the supplier for materials

Important!

Further we will reason like this. We use the cash method. First there was the receipt of materials, then payment by bank. Obviously, it is the payment by bank (since there has already been a receipt) that will create entries in columns 6 and 7. Schematically it will be like this:

receipt of materials -> will not create anything

payment by bank for materials -> fill in column 6 and column 7

Let’s enter into the program the receipt of materials in the amount of 1000 rubles:

We see that the “Income and Expenses Accounting Book” tab does not appear next to the transactions. This means that the materials receipt document in this case did not create records for any of the KUDIR columns.

We will issue a statement of payment for materials the following day:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the document has filled out columns 6 and 7:

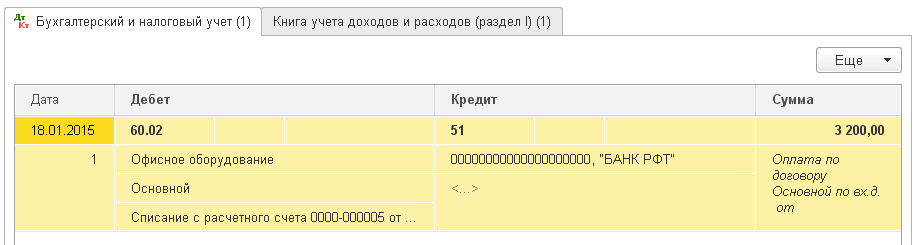

Advance payment to the supplier for the supply of materials

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

In this case, payment comes first, then materials arrive. According to the logic of the cash method, full recognition of expenses (column 7) will be possible only after both documents have been completed. Schematically it would be like this:

payment by bank for the supply of materials -> fill out column 6

receipt of materials -> fill in column 7

Let’s add into the program a statement about the prepayment for materials for 3,200 rubles:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the statement has so far filled out only column 6 (total expenses):

To fill out the seventh column, the receipt of materials document is missing. Let's format it:

We post the document and look at its postings (DtKt button):

We immediately go to the “Income and Expenses Accounting Book” tab and see that the document receipt of materials has filled in the missing column 7:

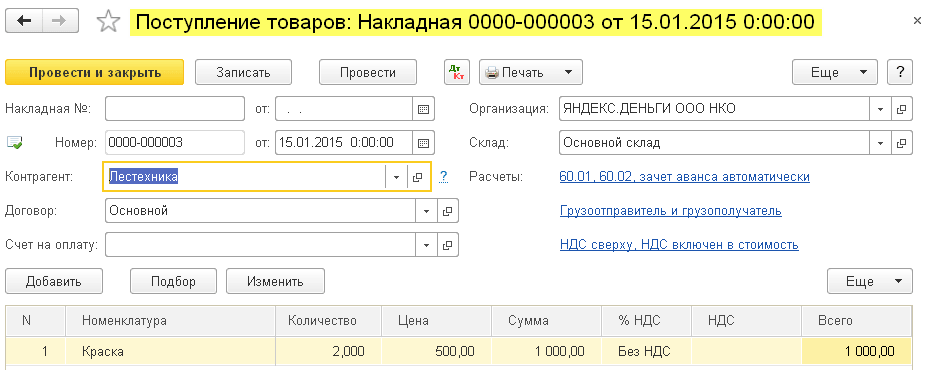

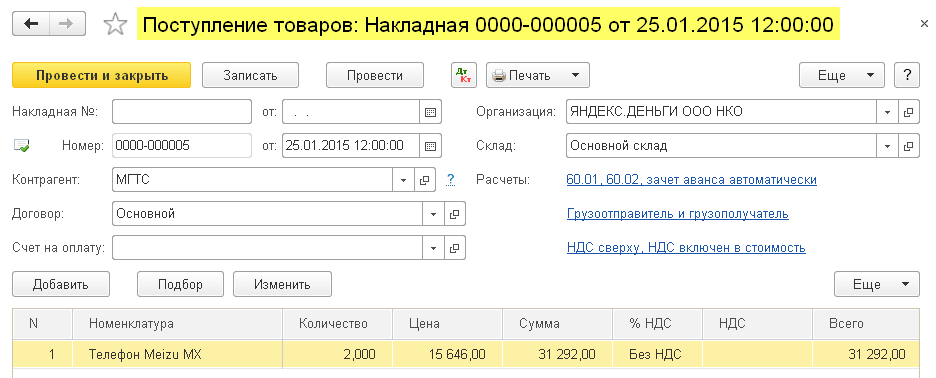

Payment to the supplier for goods

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

In general, the procedure for recognizing expenses for the purchase of goods for sale is similar to the situation with the receipt of materials - receipt and payment are also required here. But an additional (third) requirement is that expenses are recognized only as purchased goods are sold.

Schematically our scheme will be like this:

goods receipt -> fills nothing

payment for goods by bank -> fill out column 6

sales of paid goods -> fill out column 7

Let’s enter into the program the receipt of goods in the amount of 31,292 rubles:

Let’s post the document and open its postings (DtKt button):

We see that the “Income and Expense Accounting Book” tab is missing, which means the document did not record anything in the KUDIR columns.

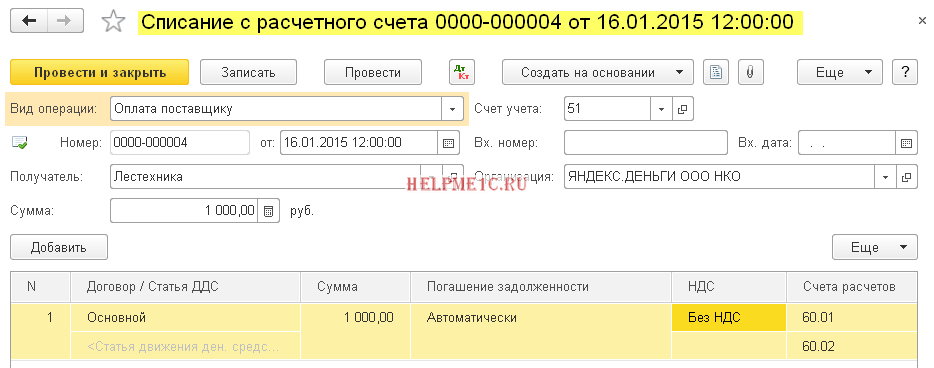

Let's enter a statement of payment for goods to the supplier:

Let’s post the document and open its postings:

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount is included in the total expenses (column 6). This amount will be included in the seventh column (expenses accepted) as the goods are sold.

Let's assume that all the goods are sold. Let's implement it:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount finally falls into the seventh column:

Advance payment to supplier for goods

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

Everything here is similar to paying the supplier for goods (previous point). Except that the payment amount will be included in the sixth column in the first document (bank statement). The scheme will be like this:

payment for goods by bank -> fill in column 6

goods receipt -> will not fill anything

sale of paid goods -> fill in column 7

Payment to the supplier through an advance report

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

If, in any of the situations described above, you replace payment by bank with payment through an accountable person, everything will work exactly the same.

But there is a nuance. The main condition for the expenses paid according to the advance report (in addition to those listed above) to be taken into account is the actual issuance of money to the accountable person (expense cash order).

Column 6 will be filled in with the RKO document.

Column 7 will be filled in when the following additional conditions occur: advance report + (act of service provision or receipt of materials or receipt of goods and their sale). Moreover, this column will be filled in with the document that is the latest in date.

Payment of wages

To fill out columns 6 and 7, you must have two documents at once: accrual and payment of wages.

Scheme 1:

payroll -> will not fill in anything

issuance of wages (RKO) -> fill in column 6 and column 7

Scheme 2:

issuance of wages before accrual (RKO) -> fill in column 6

payroll -> fill in column 7

We're great, that's all

By the way, for new lessons...

Sincerely, Vladimir Milkin(teacher and developer

Some entrepreneurs believe that there is no need to prepare advance reports under the simplified tax system. They refer to paragraph 3 of Article 4 of Law No. 129-FZ, according to which organizations and individual entrepreneurs using a simplified taxation scheme are exempt from maintaining accounting records. However, they overlook the fact that in advance reports under the simplified tax system, different entries are displayed: expenses for the purchase of goods and raw materials, travel deductions, mutual settlements with other structures, etc. Therefore, before refusing to prepare such documentation, it is advisable to first consult with specialists.

Companies that operate on a simplified taxation system have some relaxations in filing tax reports, however, advance reports under the simplified tax system of 6% are still required to be submitted. This document helps keep records of all funds that were issued to accountable persons. It must be submitted to the Federal Tax Service in a timely manner. But the specifics of registration and submission to the authority change annually. Our company employees will help you find out how advance reports are taken into account under the simplified tax system and when you need to submit the report this year. They know exactly how to properly prepare the documentation, as well as in what form to submit it to the Tax Service. They can also take on the task of compiling a report for your company.

Are advance reports necessary for the simplified tax system?

The person who received the funds on account must, no later than three days after this, present documents on the amounts spent. This official paper is called an advance payment. In the future, it will be submitted to regulatory authorities. Very often, entrepreneurs have difficulty determining how to take into account advance reports under the simplified tax system.

Difficulties with crediting funds to a single calculation arise for people who have not studied the resolutions of the Ministry of Finance. In 2017, the form for submitting this mandatory document changed, which provoked difficulties with its preparation. The new form of the advance report under the simplified tax system was approved by a resolution of the State Statistics Committee of Russia dated August 1. It was named No. AO-1.

But why do doubts so often arise whether an advance report is required under the simplified tax system? The reason for this is that companies that operate on a simplified taxation system are exempt from accounting. And the advance report should be part of this document. Therefore, many simply think that they do not need to draw up an advance report without an invoice under the simplified tax system.

However, this is a common misconception. Companies that operate on the simplified tax system of 6% must prepare advance reports. They are necessary for the enterprise, since without them it is impossible to accept expenses that were incurred by the accountable person.

For whom is accounting for advance reports under the simplified tax system mandatory?

If an entrepreneur chooses as an object of taxation income reduced by the amount of expenses, then he will have to prepare reports on advances. After all, only in this way can the costs of the relevant officials be taken into account. Recognition of advance reports under the simplified tax system is carried out if expenses:

- included in the list approved by Art. 346.16 Tax Code of the Russian Federation;

- documented;

- actually paid for by the organization.

For those organizations that use a simplified taxation scheme and choose income as its object, in many cases the recognition of expenses in advance reports under the simplified tax system and compliance with the regulations on cash transactions is mandatory. These documents indicate the amounts of cash issued to officials for business transactions.

Filling out an advance report for the simplified tax system

Reporting is a difficult and very responsible task. Therefore, not all people can cope with it. In order to correctly prepare and fill out a document, you must have special knowledge and be aware of the latest innovations. All the features of preparing an advance report under the simplified tax system are described in detail in Resolution of the State Statistics Committee of Russia No. 55.

It states that the report must be prepared in one copy by the accountable person and the company's accountant. On the reverse side you must list all the documents that confirm the expenditure of the issued funds. It can be:

- receipts;

- checks;

- transport documents.

You can find out how an advance report is prepared under the simplified tax system in 2017 from the employees of the Finabi company. Specialists constantly monitor innovations in the accounting field, so they are always aware of the latest changes. They will not only tell you how to write a report correctly, but can also complete it for you.

Nuances of drawing up advance documents

Preparing advance reports under the simplified tax system for payment of previously incurred expenses requires knowledge of accounting and relevant rules. If you are unsure whether or not to show specific expenses on your documentation, or are unsure how to show previously paid amounts of cash, also ask for help. We have thoroughly studied how an advance report is prepared under the simplified tax system for KDIR and other payments. Our employees will quickly and legally competently draw up all the papers for you, thanks to which there will be no claims against your organization from the regulatory government agencies.

When filling out a number of important points must be taken into account. First of all, each advance report under the simplified tax system must be supplemented with receipts, checks and receipt orders. Any such document:

- compiled in one copy;

- issued in paper or electronic form;

- contains a list of documents confirming costs.

If, under the simplified tax system, the advance report is not paid in accordance with the checks or the money is issued without them, then this is considered a violation. Payment documents must indicate:

- name of the purchased material assets;

- their number;

- total amount;

- date of purchase.

When to submit an advance report under the simplified tax system

Like all other mandatory declarations, the advance report must also be submitted strictly within the specified time frame. The person who received the funds on account must provide papers confirming their expenditure within 3 days after the end of the period for which they were issued. Next, the advance reports are checked under the simplified tax system. Its duration is not established by law. It all depends on the workload of the specialists who must carry out the inspection.

The accounting department is obliged to study in detail all the data specified in the report. If possible, they should check their accuracy. If the deadline for submitting the advance report under the simplified tax system is not met, then the amount may be deducted from the salary of the accountable person. Therefore, if you do not want to incur serious losses, submit documents on the spent funds in a timely manner.

It is important to remember that even individual entrepreneurs under the simplified tax system need advance reports. For them, the preparation of this document is mandatory if funds were allocated for settlements with counterparties, suppliers, or for the purchase of inventory items. The specifics of reporting for companies and individual entrepreneurs are no different.

Advance reports for UTII are also required. Even a single tax on imputed income does not exempt you from drawing up this document. Therefore, it can be argued that absolutely all enterprises that operate under any taxation regime must prepare and submit advance reports.

Overexpenditure in the advance report under the simplified tax system

Situations often arise when the amount issued by the enterprise is simply not enough to purchase all the necessary goods or pay for services. In this case, it becomes difficult to reflect the overexpenditure of funds in the report. This fact must be indicated in the detailed list of expenses incurred. After checking the document, management will issue a refund according to the advance report under the simplified tax system.

If the accountable person has funds left, then he is obliged to hand them over to the cashier. If the employee has not repaid the unspent funds, then the manager will withhold the amount of the debt from his salary.

Electronic advance report

In accordance with the current tax legislation and guidelines of the Ministry of Finance of the Russian Federation, advance reports under the simplified tax system of 15% and other similar taxation systems can be submitted to the appropriate services in both paper and electronic versions. The main thing is that they reflect reliable information, and their design complies with the requirements of the regulations. Under the simplified tax system 8 2, advance reports on computer media must contain a certified electronic signature. These documents must display all funds issued in cash or previously paid to:

- all business transactions performed;

- purchase of materials or goods;

- travel expenses for staff.

The organization applies a simplified system with the object of taxation being income minus expenses. The employee purchased a computer for the office with his own money, brought payment documents and wrote an application asking for reimbursement of expenses. I submitted an advance report, but now there is no money to pay for the purchase. Is it possible to take into account the cost of a computer if it has already been put into operation?

16.09.2009Magazine "Simplified"

Undesirable consequences

In this case, the cost of the computer can be included in expenses only after the debt to the employee is paid off. Moreover, tax authorities may not accept the advance report and decide that the employee sold the computer to the organization. If this happens, you will have to pay additional personal income tax.

The general rules for issuing cash on account are specified in paragraphs 10 and 11 of the Procedure for conducting cash transactions, approved by decision of the Board of Directors of the Central Bank of the Russian Federation dated 22.0993 No. 40 (hereinafter referred to as the Procedure).

Firstly, the head of the enterprise must set in the order the period for which the money is issued. This is due to the fact that, according to paragraph 11 of the Procedure, the employee is obliged to report on his expenses within three working days after the appointed deadline, and if the deadline is not set, he is given only three working days after receiving the amount. In case of delay, tax authorities may consider that the employee was given an interest-free loan and charge personal income tax on the material benefit. Yes, this can be challenged, but it is easier to issue an order. In addition to the deadline, tax officials recommend providing a list of employees who will take accountable money. There is no such requirement in the Order, but it is quite appropriate, and it is not difficult to fulfill.

Secondly, an employee can receive another advance only if he has closed the previous one.

Thirdly, it is unacceptable to transfer accountable amounts. For example, if one employee was unable to buy a product and this was entrusted to another, then the first must return the money to the cash register, and the second must take it.

Let's move on to accounting. Under the simplified system, the tax base can be reduced only for expenses incurred and paid (clause 2 of Article 346.17 of the NKRF). Your employee purchased a computer for the company. The write-off procedure depends on the amount paid.

Let us remind you that you can only take into account those types of expenses that are indicated in the list of paragraph 1 of Article 346.16 of the NKRF. Subclause 1 indicates the cost of purchase, manufacture or construction of fixed assets. They include property recognized as depreciable in accordance with Chapter 25 of the NKRF (clause 4 of Article 346.16 of the NKRF). Paragraph 1 of Article 256 of the NKRF states that depreciable objects are those with a useful life of more than 12 months and more expensive than 20,000 rubles, which are owned and used to generate income. It agrees with the first three signs: the computer belongs to the organization, allows you to generate income and is designed for more than a year of operation. Even if it costs more than 20,000 rubles, it can be classified as fixed assets. Expenses on them are reflected in equal shares for the quarters remaining until the end of the tax period, after payment and commissioning of the facilities (clause 3 of Article 346.16 and subclause 4 of clause 2 of Article 346.17 of the NKRF).

If the computer cost 20,000 rubles. or less, it can no longer be called depreciable and it is not a fixed asset. However, the purchase costs can still be taken into account in the tax base. According to subclause 5 of clause 1 of Article 346.16 of the NKRF, it is allowed to reflect material expenses, and in accordance with Article 254 of the NKRF, they include the cost of non-depreciable property (subclause 3 of clause 1). It can be written off after payment and commissioning of the facility (subclause 3, clause 1, article 254 and clause 2, article 346.17 of the NKRF).

Apparently, the computer is already in use, although the employee has not been paid. This means that the organization did not pay the expenses, and until this happens, it will not be possible to take into account the expenses. Something else is more important.

As has been said more than once, tax authorities do not like reverse reporting. Why? The employee spent his own money and then transferred the property to the organization. Tax inspectors have the right to regard this as resale. Accordingly, they will include the proceeds in the employee’s taxable income and increase personal income tax. Of course, you shouldn’t agree with the tax authorities, but in any case, an extra burden falls on the accountant.

What can be changed

Check whose name the invoice is issued in. If the name of the organization is indicated, then everything is in order, if not, it is worth re-issuing the document. However, it is better to do without reporting on the contrary, but to enter into an interest-free loan agreement with the employee for an amount equal to the cost of the computer.

The documents issued to the employee should be redone. Otherwise, firstly, it will not be possible to recognize the cost of the computer as an expense - how to confirm that it was the organization that purchased the property? And secondly, this gives grounds to consider the transfer of a computer by an employee as a resale and to charge additional personal income tax on his income. So it’s easier to contact the store with a request to change the document. If the buyer is not indicated at all on the sales receipt, we advise you to play it safe and ask to indicate the name of the organization.

At the same time, even correctly completed purchase documents may not convince the tax authorities. We suggest taking a different path. Enter into an interest-free loan agreement with the employee for an amount equal to the cost of the computer. What conditions it should contain are set out in Articles 807-813 of the Civil Code of the Russian Federation. Then, on the same day, formalize the receipt of money from the employee at the cash desk under the loan agreement and issue it to him on account. Attach documents proving the purchase of the computer to the advance report, and the advance will be closed. You can repay the debt to the employee at any time no later than specified in the loan agreement.

What are the advantages of this option? First of all, the cost of the computer can be taken into account before the debt to the employee has been repaid. Indeed, according to paragraph 1 of Article 807 of the Civil Code of the Russian Federation, borrowed amounts are considered the property of the borrower. Consequently, the organization paid for the computer with its own money and after putting it into operation, you can write off its cost as expenses in quarterly equal shares until the end of the tax period (clause 3 of Article 346.16 and subclause 4 of clause 2 of Article 346.17 of the NKRF) or at a time, if the computer costs 20,000 rubles. and cheaper (subclause 5, clause 1, article 346.16 and clause 2, article 346.17 of the NKRF). Please note that neither the receipt nor the repayment of the loan is reflected in tax accounting. Borrowed funds are non-taxable income (subclause 10, clause 1, article 251 of the NKRF), and a repaid loan under the simplified system is not recognized as an expense - it is not mentioned in the closed list (clause 1, article 346.16 of the NKRF).

But most importantly, the advance report will be flawless and the reason for disagreements with the tax authorities will disappear.

There seems to be no doubt that under the simplified system, borrowed funds are not taken into account. According to subparagraph 1 of paragraph 1.1 of Article 346.15 of the NKRF, income listed in Article 251 of the NKRF is not included in the tax base. And in subparagraph 10 of paragraph 1 of Article 251 of the NKRF, the amounts received under the loan agreement are indicated. And yet, sometimes tax authorities determine income based on bank statements alone, and borrowed funds are subject to taxation. True, the courts stop this. Thus, the Supreme Arbitration Court of the Russian Federation confirmed (Determination No. 13467/08 dated October 16, 2008) that the money that the taxpayer had was borrowed and its amount should not be included in taxable income. This means that the inspection brought the organization to justice without justification. Similar facts were considered by the Federal Antimonopoly Service of the Moscow District (resolution dated April 2, 2008 No. KA-A40/2446-08). Here, the judges also supported the taxpayer, who returned the loan and did not want to pay tax on it.

If the loan amount is small, the tax authorities simply charge additional taxes (as well as penalties and fines). Those whose income together with the loan exceed the maximum permissible level (clause 4 of Article 346.13 of the NKRF) are treated differently. Let us remind you that the current limit is 30.76 million rubles. (20 million rubles, multiplied by a deflator coefficient of 1.538). Next year it is planned to raise it to 60 million rubles. (the bill passed the second reading in the State Duma). So, tax authorities do not increase the single tax, but force them to pay taxes provided for under the general regime.

In the courts, it again turns out that the disputed funds included in the income were borrowed. This means that the maximum level was observed. This decision is contained in the resolutions

What the courts say

FAS of the Central District dated 01.28.2009 No. A09-4405/2008-15, North Caucasus District dated 09.30.2008 No. F08-5821/2008 and dated 07.02.2008 No. F08-3717/2008, Ural District dated 06.09.2008 No. F09 -4103/08-С3 and the North-Western District dated 06/30/2008 No. A21-355/2008. True, in the case with which the latest resolution is connected, the loan received was incorrectly reflected in accounting, which gave the tax authorities a reason to attribute its amount to income. However, according to the judges, errors in recording transactions in accounting accounts cannot affect the right to apply the simplified system.

The deflator coefficient for 2009 was established by order of the Ministry of Economic Development of Russia dated November 12, 2008 No. 395

Pay attention to the circumstances examined by the Federal Antimonopoly Service of the Volga-Vyatka District (resolution dated October 17, 2007 No. A82-1474/2007-28). An individual entrepreneur using the simplified tax system took out an interest-free loan. During the audit, the tax authorities stated that the borrower had generated income in the form of material benefits and additionally assessed personal income tax. However, relying on paragraph 3 of Article 346.11 of the Tax Code of the Russian Federation, the judges considered that the entrepreneur should not pay personal income tax on income from business activities, and canceled the decision of the tax inspectorate.

This refers to the wording in force until 2009

We highlighted this case because the entrepreneur would not win it now. On January 1, 2009, a new version of paragraph 3 of Article 346.11 of the Tax Code of the Russian Federation came into force, according to which, under the simplified system, personal income tax is still not withheld from the income of an entrepreneur, but only if they are not taxed at the rates specified in paragraphs 2, 4 and 5 of Article 224 Tax Code of the Russian Federation. And in paragraph 2, savings on interest on borrowed funds are mentioned. Let us repeat, we are talking only about individual entrepreneurs. Organizations do not take such income into account, which is confirmed by the Ministry of Finance (see letter dated 04/02/2007 No. 03-11-04/2/78).

What will be the accounting entries for the advance report, the procedure for reflecting overexpenditures, etc.?

DESCRIPTION OF THE SITUATION: On June 5, 2017, an employee of an organization using the simplified tax system received 2,000 rubles as a report. to buy a printer cartridge. On June 8, 2017, an employee purchased a cartridge for 2,500 rubles. (excluding VAT) and brought an advance report to the company’s accounting department. The company employee attached a sales receipt and a cash register receipt for the purchase of a cartridge to the advance report. On June 9, 2017, the director of the company approved the report, the company capitalized the cartridge and immediately put it into operation, installing it on the printer. On June 10, 2017, the cashier accountant gave the accountant the amount of overexpenditure on the advance report in the amount of 500 rubles. (2500 rub. – 2000 rub.).

QUESTION: How and when can the cost of a cartridge be included in expenses?

ANSWER:The employee who received the money on account must submit an advance report on the amounts spent (Form No. AO-1).

The employee returns the unspent money, i.e. the balance on the advance report, to the cashier.

If more money is spent than issued, the overexpenditure, with the consent of the manager, is reimbursed to the employee.

In accounting, these transactions are reflected as follows:

|

Wiring |

Operation |

|

On the date of issue of money for reporting |

|

|

Debit 71 - Credit 50 |

The employee was given money on account |

|

As of the date of approval of the advance report |

|

|

Debit 10 (08, 20, 26, 44) - Credit 71 |

Goods (work, services) paid for by the accountable have been accepted for accounting. For example, stationery, notary services, travel expenses |

|

Debit 50 - Credit 71 |

The balance of unspent accountable money was received from the employee |

|

Debit 71 - Credit 50 |

The overexpenditure on the advance report was returned to the employee |

|

Payments using a plastic card |

|

|

Debit 55 - Credit 51.52 |

The employee has been allocated funds to spend using a corporate card |

|

Debit 71 - Credit 55 |

An employee withdrew money from a corporate card (the employee was given funds on account) |

|

Debit 73- Credit 55 |

The write-off of cash from a special account, not confirmed by primary documents, is reflected |

|

Debit 50 - Credit 73 |

Cash contributed by the employee to reimburse expenses |

|

Debit 70 - Credit 73 |

The amount of money spent on a corporate card for personal purposes is withheld from the employee’s salary |

Features for simplified tax system

For payers of the simplified tax system with the object “income minus expenses,” only paid expenses are reflected in the tax base under the simplified tax system. And they will be considered paid when the company has no debt (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

When overspending occurs, the organization incurs a debt to the employee.

Therefore, it is incorrect to take into account expenses until it is repaid.

Expenses are considered paid when the organization has issued the overage amount to the employee.

This is also confirmed by the explanations of the Ministry of Finance. As noted in the letter of the Ministry of Finance of Russia dated January 17, 2012 No. 03-11-11/4, when an employee of an organization purchases inventory items at his own expense, their cost can be taken into account as expenses in the reporting period for repaying the organization’s debt to the employee.

Therefore, if the organization has settled with the accountable party, fulfilled other conditions and has supporting documents, then the entire amount of expenses can be written off.

If the amount of overexpenditure is reimbursed to the employee in the next quarter, then to write off expenses under the simplified tax system, you can not wait for full payment, but proceed as follows:

- write off the purchase price minus overruns immediately after approval of the expense report;

- the remaining balance is written off on the day the organization pays the amount due to the employee.

Of course, it is necessary to have supporting documents and comply with other necessary conditions (clause 2 of Article 346.16 and clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

Since the Organization has paid off with the accountable, fulfilled other conditions and has supporting documents, in this case, the organization has the right to reflect the cost of a printer cartridge in material expenses immediately after posting the property and payment (subclause 5, clause 1, article 346.16, subclause 1 clause 2 of article 346.17 of the Tax Code of the Russian Federation).

The cartridge was capitalized on June 9, 2017, and paid in full on June 10, 2017 - after the debt to the employee was repaid.

The employee attached a cash register receipt to the report.

These documents are sufficient to record expenses.

Therefore, on June 10, 2017, the organization will enter in column 5 of the book of income and expenses the cost of the cartridge - 2,500 rubles.

The accounting entries will be as follows.

Debit 71 Credit 50

- 2000 rub. - money was issued on account to an employee of the company;

Debit 10 Credit 71

- 2500 rub. - the cartridge purchased by the accountant has been capitalized;

Debit 26, 44 Credit 10

- 2500 rub. - the printer cartridge is decommissioned;

Debit 71 Credit 50

- 500 rub. - the amount of overexpenditure according to the advance report was issued to the company employee.

Implementation of purchases of inventory items, settlements with counterparties- these are just some of the situations in which an advance report is drawn up. However, “simplistic people” sometimes believe that there is no point in bothering with the preparation of additional documents.

How legitimate is this position of taxpayers? What points should you pay attention to when drawing up an advance report and when assigning expenses on it to expenses when calculating the single tax paid? when using the simplified tax system?

Or maybe we can get by?

Of course, before talking about all the controversial issues that arise during the process, it is necessary to decide on the main question: a Does a "simplified" person need an advance report?? After all, according to paragraph 3 of Art. 4 of Federal Law N 129-FZ (Federal Law of November 21, 1996 N 129-FZ “On Accounting”) “simplified people” are exempt from accounting. And if organizations that have chosen income reduced by the amount of expenses as an object of taxation can somehow explain to themselves that they need this primary document, then the “simplified” with the object of taxation “income” are sometimes completely sure: not like advance reports , and in general they don’t need most (or even all) of the primary documents, because the tax is calculated on income, determined by the cash method, that is, from the receipt of funds to current accounts and to the cash desk, which is not difficult to verify.

However, the situation is not as simple as it might seem at first glance.

Let's start with the “simplified people” who chose the object of taxation "income reduced by expenses". In this case, drawing up an advance report is simply necessary. After all, otherwise it is impossible to accept as expenses the costs incurred by the accountable person.

Let us turn to the provisions of Ch. 26.2 Tax Code of the Russian Federation.

Expenses are recognized if they:

1) are included in the list of expenses given in Art. 346.16 Tax Code of the Russian Federation;

2) comply with Art. 252 Tax Code of the Russian Federation: documented and economically justified. And here we first encounter the requirement for documentation. But it is the expense report that is the primary document. Train tickets, plane tickets and sales receipts cannot in themselves confirm expenses, and only when prepared with an expense report do such expenses acquire a high expense status. This is exactly what is stated in the Letter of the Federal Tax Service of Russia dated April 23, 2007 N 18-11/3/037127.1@: documents confirming the validity of the expenses incurred by the taxpayer are:

- cash order;

- order (instruction) on sending an employee (workers) on a business trip in form N T-9 (T-9a), approved by Resolution of the State Statistics Committee of Russia dated January 5, 2004 N 1;

- travel certificate in form N T-10, approved by Resolution of the State Statistics Committee of Russia dated January 5, 2004 N 1;

- official assignment for sending on a business trip and a report on its implementation in form N T-10a, approved by Resolution of the State Statistics Committee of Russia dated January 5, 2004 N 1;

- advance report of the posted employee in Form N AO-1, approved by Resolution of the State Statistics Committee of Russia dated 01.08.2001 N 55, with the attachment of relevant supporting documents confirming the actual expenses incurred by him for travel, accommodation, etc., approved by the manager;

3) paid by the organization. This is another condition that “simplified” people who apply the simplified tax system with the object “income minus expenses” should not forget about. Thus, if reporting is carried out in the classic version, that is, first the accountable person received the money and then reported for the funds received, the date of recognition of expenses will be the date of approval of the advance report, since it is at this moment that all the conditions necessary for accepting expenses are met: they are paid (at the moment when funds are issued on account) and produced (as evidenced by the report of the accountable person). A similar position is expressed by specialists from the main financial department (see, for example, Letter dated 02/16/2011 N 03-11-06/2/21): paragraphs. 13 clause 1 art. 346.16 of the Code establishes that taxpayers have the right to take into account travel expenses when determining the tax base, in particular for the rental of living quarters, payment of daily allowances, etc. However, reducing the tax base for these expenses at the start of a business trip is illegal, since the advance report is submitted only after its completion.

In view of the above, having issued an advance to the employee for travel expenses, the taxpayer does not have the right to include it in expenses until it is spent on the purpose of the business trip(purchase of travel documents, hotel accommodation, etc.) and documented(advance report with supporting documents attached).

In a case that is quite common in practice, when an employee of an organization (usually a manager) first acquires the necessary inventory items, and then submits an expense report and receives reimbursement for it, the moment of recognition of expenses will be the moment of reimbursement of overexpenses according to the expense report.

Now let's move on to those organizations that apply the simplified tax system with the object of taxation "income". Do such taxpayers need to prepare advance reports?

Tax service specialists have repeatedly provided their explanations on this issue.

Based on Art. 9 of Federal Law N 129-FZ, all business transactions carried out by an organization must be documented with supporting documents, which serve as primary documents.

Primary documents are accepted for accounting if they are drawn up in accordance with the form contained in the albums of unified forms of primary accounting documentation. At the same time, documents whose form is not provided for in these albums must contain the mandatory details established by Art. 9 of Federal Law N 129-FZ.

In accordance with paragraph 4 of Art. 346.11 of the Tax Code of the Russian Federation, for organizations and individual entrepreneurs using the simplified tax system, the current procedure for conducting cash transactions is preserved.

Resolution of the Goskomstat of the Russian Federation N 88 (Resolution of the Goskomstat of Russia dated August 18, 1998 N 88 “On approval of unified forms of primary accounting documentation for recording cash transactions, accounting for inventory results”) for accounting cash transactions, the following unified forms of primary accounting documentation were approved:

- cash receipt order (form N KO-1);

- expense cash order (form N KO-2);

- journal of registration of incoming and outgoing cash documents (form N KO-3);

- cash book (form N KO-4);

- book of accounting of funds accepted and issued by the cashier (form N KO-5).

According to paragraphs 3 and 11 of the Procedure for conducting cash transactions in the Russian Federation (Approved by the Decision of the Board of Directors of the Central Bank of the Russian Federation dated September 22, 1993 N 40), in order to make cash payments, each enterprise must have a cash desk and maintain a cash book in the prescribed form.

Enterprises issue cash on account for business and operating expenses in amounts and for periods determined by enterprise managers. Persons who received cash on account are obliged, no later than three working days after the expiration of the period for which they were issued, to submit a report on the amounts spent to the accounting department of the enterprise and make a final payment for them.

For settlements with accountable persons, a unified primary document is provided - an advance report, the form of which is approved by Resolution of the State Statistics Committee of Russia dated N 55 (Resolution of the State Statistics Committee of Russia dated 01.08.2001 N 55 "On approval of the unified form of primary accounting documentation N AO-1 "Advance report").

The verified expense report is approved by the manager or an authorized person and accepted for accounting. Based on the data of the approved advance report, the accounting department writes off the accountable amounts in the prescribed manner.

This position is presented in Letters of the Federal Tax Service for Moscow dated January 18, 2007 N 18-11/3/03895@, dated December 21, 2005 N 18-11/3/94150.

Thus, organizations using the simplified tax system with the object of taxation “income” are required to comply with the Procedure for conducting cash transactions and, therefore, draw up advance reports. At the same time, this justification in favor of drawing up advance reports is suitable for all “simplified” people, including those who have chosen the object “income minus expenses”, however, as we said earlier, the latter have a stronger argument for drawing up advance reports - the need accounting and recognition of expenses.

Advance report: main points of filling out

Briefly about the main thing

Resolution of the State Statistics Committee of Russia No. 55 provides Key points you need to know when filling out an expense report. Let's recall some of them:

- an advance report is used to account for funds issued to accountable persons for administrative and business expenses;

- the advance report is drawn up in one copy by the accountable person and the accounting employee;

- an advance report can be drawn up on paper and computer media;

- on the reverse side of the form, the reporting person provides a list of documents confirming the expenses incurred (travel certificate, receipts, transport documents, cash register receipts, sales receipts and other supporting documents), and the amount of expenses for them (columns 1 - 6). The documents attached to the advance report are numbered by the accountable person in the order in which they are recorded in the report;

- the accounting department checks the intended use of funds, the presence of supporting documents confirming the expenses incurred, the correctness of their execution and calculation of amounts, and also on the reverse side of the form the amounts of expenses accepted for accounting are indicated (columns 7 - 8), and accounts (sub-accounts) that debited for these amounts (column 9);

- details related to foreign currency (line 1a of the front side of the form and columns 6 and 8 of the back side of the form) are filled in only if funds are issued to the accountable person in foreign currency in accordance with the established procedure in accordance with the current legislation of the Russian Federation;

- the verified expense report is approved by the manager or an authorized person and accepted for accounting. The balance of the unused advance is handed over by the accountable person to the organization's cash desk using a cash receipt order in the prescribed manner. Overexpenditure on the advance report is issued to the accountable person according to the cash receipt order;

- based on the data of the approved advance report, the accounting department writes off accountable amounts in the prescribed manner.

Advance report in electronic form: is it possible?

Clauses 1 and 2 of Art. 1 of Federal Law No. 1-FZ (Federal Law of January 10, 2002 No. 1-FZ “On Electronic Digital Signature”, valid until July 1, 2012 along with Federal Law of April 6, 2011 No. 63-FZ “On Electronic Signature”) It has been determined that an electronic digital signature in an electronic document is recognized as equivalent to a handwritten signature in a paper document. The effect of this Federal Law extends to relations arising during civil transactions and in other cases provided for by the legislation of the Russian Federation.

Will expense reports (standard form N AO-1), issued in electronic form and signed with an electronic digital signature, confirm the organization’s expenses?

The opinion of the main financial department on this issue is presented in Letter dated January 11, 2011 N 03-03-06/1/3.

In accordance with paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, expenses are recognized as justified and documented expenses (and in cases provided for in Article 265 of the Tax Code of the Russian Federation, losses) incurred (incurred) by the taxpayer.

Justified expenses mean economically justified expenses, the assessment of which is expressed in monetary form. Documented expenses mean expenses supported by documents drawn up in accordance with the legislation of the Russian Federation. Any expenses are recognized as expenses, provided that they are incurred to carry out activities aimed at generating income.

According to paragraphs 1, 2 and 7 of Art. 9 of Federal Law N 129-FZ, all business transactions carried out by an organization must be documented with supporting documents. These documents serve as primary accounting documents on the basis of which accounting is conducted.

Primary accounting documents are accepted for accounting if they are drawn up in the form contained in the albums of unified forms of primary accounting documentation, and documents whose form is not provided for in these albums must contain the mandatory details established by paragraph 2 of Art. 9 of the above Law.

Primary and consolidated accounting documents can be compiled on paper and computer media. In the latter case, the organization is obliged to produce, at its own expense, copies of such documents on paper for other participants in business transactions, as well as at the request of the authorities exercising control in accordance with the legislation of the Russian Federation, the court and the prosecutor's office.

Clauses 1 and 2 of Art. 1 of Federal Law No. 1-FZ establishes that the purpose of this Law is to ensure legal conditions for the use of electronic digital signatures in electronic documents, subject to which an electronic digital signature in an electronic document is recognized as equivalent to a handwritten signature on paper.

The effect of this Law extends to relations arising during civil transactions and in other cases provided for by the legislation of the Russian Federation.

In accordance with paragraph 3 of Art. 11 of Federal Law N 149-FZ (Federal Law of July 27, 2006 N 149-FZ “On Information, Information Technologies and Information Protection”) an electronic message signed with an electronic digital signature or another analogue of a handwritten signature is recognized as an electronic document equivalent to a document signed with a handwritten signature, in cases where federal laws or other regulatory legal acts do not establish or imply a requirement to draw up such a document on paper.

Thus, a document executed in electronic form and signed with an electronic digital signature may be a document confirming expenses incurred by the taxpayer in cases where federal laws or other regulatory legal acts do not establish or imply a requirement for the preparation of such a document on paper.

Accounting for the costs of purchasing forms of primary documents

Today, most organizations keep records in specialized programs, which also make it possible to print relevant documents with information already entered into them. However, the issue of accounting for the costs of purchasing document forms, including advance report forms, remains relevant for some taxpayers, and confirmation of this is the explanation of officials of the main financial department. When asked which expense item should be used to reflect the cost of advance reports acquired by banks, financiers answer: taking into account the fact that, in accordance with paragraphs. 17 clause 1 art. 346.16 of the Code, when determining the object of single taxation, expenses for office supplies are taken into account; the taxpayer has the right to reduce the income received by expenses for paying the cost of purchased forms (Letter dated May 17, 2005 N 03-03-02-04/1/123).

Supporting documents: various situations

A separate point in the large topic called “Advance report” is the question of supporting documents that are attached to the advance report. As a rule, accountants of organizations require sales and cash receipts from their accountants. What to do, if there is no cash receipt? When checking, the Federal Tax Service qualifies such amounts as the income of the employee to whom the advance report was issued and tries to impose personal income tax. Judges side with taxpayers on this issue. This is precisely the situation considered in the Resolution of the Federal Antimonopoly Service of the Far East of July 26, 2006, July 19, 2006 N F03-A73/06-2/1776.

As follows from the case materials, the company issued sums of money to its employees on account for the purchase of flowers for anniversaries and special events. In confirmation of the expenditure of the funds issued on account for the specified purposes, sales receipts were presented, as well as acts on the acquisition of inventory items drawn up by employees of the tax agent, which cannot replace the primary accounting documents, namely a cash receipt.

In accordance with Art. 9 of Federal Law N 129-FZ, all business transactions carried out by an organization must be documented with supporting documents on the basis of which accounting records are kept.

Primary accounting documents are accepted for accounting if they are drawn up in the form contained in the albums of unified forms of primary accounting documentation, and documents whose form is not provided for in these albums must contain the mandatory details listed in this article.

In pursuance of this Law, the Government of the Russian Federation adopted Resolution No. 835 of 07/08/1997 “On primary accounting documents”, according to which Goskomstat is entrusted with the functions of developing and approving unified forms of primary accounting documentation.

Resolution of the State Statistics Committee of the Russian Federation No. 55 approved the unified form of primary accounting documentation AO-1 “Advance report” with instructions for its use and completion (put into effect on January 1, 2002). This form is used to account for funds issued to accountable persons for administrative and business expenses.

In accordance with these instructions, the organization’s accounting department checks the intended use of funds, the availability of supporting documents confirming the expenses incurred, the correctness of their execution and calculation of amounts. At the same time, the list of documents confirming expenses includes: receipts, transport documents, cash register receipts, sales receipts and other supporting documents. That is, such a list is not exhaustive.

Thus, the absence of a cash register receipt in the presence of other supporting documents cannot be unconditional evidence of misuse of funds by accountable persons and the latter’s receipt of income subject to personal income tax.

The judges of the Far Eastern District are supported in this matter by their colleagues from the West Siberian District: the inspectorate’s reference to the absence of cash receipts as documentary evidence of the advance report was rightfully rejected by the arbitration court, since the sales receipt issued in accordance with the requirements of Art. 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting” is a document of primary accounting documentation, and the absence of cash receipts does not indicate that the accountable person spent money on his own needs. In addition, the court found that material assets were purchased in cash for production needs and were taken into account as fixed assets.

The totality of the above circumstances indicates the correctness of the arbitration court’s conclusion that an individual has no income and, therefore, that there are no grounds for holding the company liable for incomplete payment of personal income tax (Resolution dated September 20, 2007 N F04-2603/2007(38159-A81-7) ).

As a separate topic, we can highlight the issue related to confirmation of expenses by accountable persons in the case when inventory items are purchased by accountable persons from UTII payers. This is due to the changes made to Federal Law No. 54-FZ (Federal Law No. 54-FZ of May 22, 2003 “On the use of cash register equipment when making cash payments and (or) settlements using payment cards”). According to these changes, UTII payers who are not subject to clauses 2 and 3 of Art. 2 of Federal Law No. 54-FZ, when carrying out types of business activities established by clause 2 of Art. 346.26 of the Tax Code of the Russian Federation, can carry out cash payments and (or) payments using payment cards without the use of cash register equipment, provided that, at the request of the buyer (client), a document (sales receipt, receipt or other document) is issued confirming the receipt of funds for the corresponding product (work, service). Can “simplifiers” use this document to confirm expenses incurred?

In Letter dated October 15, 2010 N 03-11-06/2/156, financiers provide the following explanations on this issue. In accordance with paragraph 2 of Art. 346.16 of the Tax Code of the Russian Federation, taxpayers applying the simplified taxation system and choosing as an object of taxation income reduced by the amount of expenses, when calculating the tax base, have the right to take into account the expenses provided for in paragraph 1 of this article and meeting the criteria of paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, that is, justified, documented expenses incurred to carry out activities aimed at generating income.

Article 346.24 of the Tax Code of the Russian Federation establishes that taxpayers using the simplified tax system are required to keep records of income and expenses for the purpose of calculating the tax base for the tax in the book of income and expenses of organizations and individual entrepreneurs using the simplified taxation system, the form and procedure for filling which are approved by the Ministry of Finance.

In accordance with Order of the Ministry of Finance of Russia N 154n (Order of the Ministry of Finance of Russia dated December 31, 2008 N 154n “On approval of the forms of the Book of accounting of income and expenses of organizations and individual entrepreneurs using a simplified taxation system, Book of income of individual entrepreneurs using a simplified taxation system based on a patent , and the Procedure for filling them out"), transactions recorded in the accounting books must be confirmed by primary documents.

Thus, for taxpayers of the simplified taxation system, confirmation of the amount of expenses for payment for purchased goods (work, services), regardless of the amount, is provided by primary documents (payment documents, acceptance certificates, invoices, concluded contracts, etc.).

By virtue of clause 2.1 of Art. 2 of Federal Law N 54-FZ organizations and individual entrepreneurs who are payers of the single tax on imputed income for certain types of activities that are not subject to clauses 2 and 3 of Art. 2 of Federal Law No. 54-FZ, when carrying out types of business activities established by clause 2 of Art. 346.26 of the Tax Code of the Russian Federation, can carry out cash payments and (or) payments using payment cards without the use of cash register equipment, provided that, at the request of the buyer (client), a document (sales receipt, receipt or other document) is issued confirming the receipt of funds for the corresponding product (work, service).

Thus, the corresponding expenses when making cash payments and (or) payments using payment cards in cases of sale of goods, performance of work or provision of services must be confirmed by cash receipts or documents printed by cash register equipment (sales receipts, receipts or other documents), confirming the receipt of funds for the relevant product (work, service).

The specified documents containing the information provided for in clause 2.1 of Art. 2 of Federal Law N 54-FZ, can be issued by organizations and individual entrepreneurs who are payers of UTII for certain types of activities, when they carry out relevant business activities that are subject to UTII for certain types of activities.

Advance report from the employee's point of view

As for the employee, a sore point for both parties may be the situation when the employee has not accounted for the funds received under the report. What should the organization do? Is it possible to withhold unspent funds from an employee’s salary? How to document this operation?

Typical situation. The employee of the organization was on a business trip. He spent less money than he received on account. He did not return the remaining unspent funds to the cash register. The organization decided to withhold this amount from his salary. Do you need an order from the director for this, or can the accounting department do it independently (for example, based on an expense report)? Should an employee write a statement asking for money to be withheld from his salary?

As Rostrud specialists note in Letter No. 3044-6-0 dated 08/09/2007, upon returning from a business trip, an employee is required to draw up an advance report in the form approved by Resolution of the State Statistics Committee of Russia No. 55. The balance of the unused advance is handed over by the accountable person to the organization’s cash desk using a cash receipt order according to established order.

If the employee does not promptly return the balance of unused funds to the cashier, Art. 137 of the Labor Code of the Russian Federation, which provides for cases of deduction from an employee’s salary to repay his debt to the employer.

In particular, deductions from an employee’s salary to pay off his debt to the employer can be made to repay an unspent and not returned timely advance payment issued in connection with a business trip. In this case, the employer has the right to decide to deduct from the employee’s salary no later than one month from the date of expiration of the period established for the return of the advance, and provided that the employee does not dispute the grounds and amount of the deduction.

The employer makes and formalizes decisions, as a rule, in the form of an order or instruction, although a unified form of such an order is not established by regulatory legal acts.

As for the employee's consent to withhold amounts from wages, it should be obtained in writing.